Table of contents

Homeowners often hear about the “mortgage interest deduction,” but the actual rules are more nuanced than many people realize. Whether the deduction benefits you depends on the type of property you own and how you file your taxes.

Below is a practical overview of how mortgage interest deductions work.

Mortgage Interest on a Primary Residence or Second Home

Mortgage interest paid on a primary residence or second home may be deductible as an itemized deduction on Schedule A.

However, two important conditions apply.

1. You must itemize deductions

Mortgage interest only provides a tax benefit if you itemize deductions. If you take the standard deduction, the mortgage interest does not reduce your taxable income.

Current standard deductions are approximately:

- Married Filing Jointly: about $29,000

- Single: about $14,600

If your total itemized deductions are lower than the standard deduction, itemizing usually provides no additional benefit.

2. Loan size limits apply

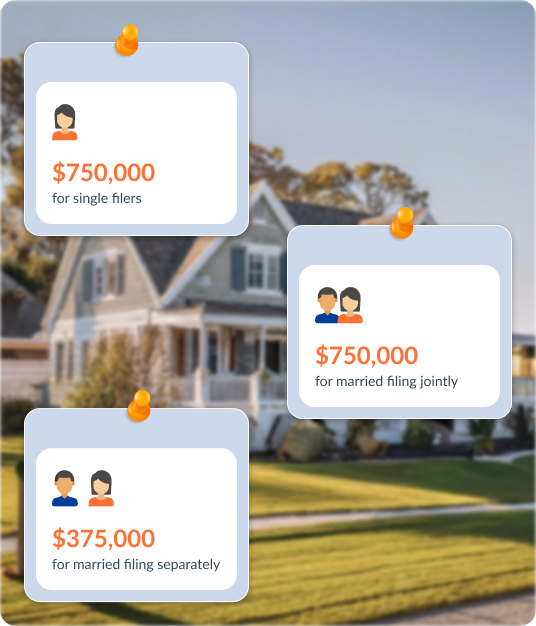

Mortgage interest deductions apply only to interest paid on loans up to:

- $750,000 for Single filers

- $750,000 for Married Filing Jointly

- $375,000 for Married Filing Separately

This rule applies to loans originated after December 15, 2017.

Married couples filing separately cannot double the limit. The cap applies across the household.

Other Itemized Deductions Homeowners May Claim

In addition to mortgage interest, homeowners may also deduct:

- Property taxes

- Mortgage points

- Certain prepaid interest

However, property taxes fall under the SALT deduction limit, which caps the total amount of state and local taxes that can be deducted.

SALT Deduction Limits

The SALT deduction includes:

- Property taxes

- State income taxes

- Local taxes

Through 2024, the deduction is limited to $10,000 per household.

Starting in 2025:

- The cap increases to $40,000

- Phaseout begins at $500,000 income

- The cap increases roughly 1% annually through 2029

- It is scheduled to revert to $10,000 in 2030 unless extended

Importantly, the SALT cap does not affect mortgage interest deductions. It only applies to taxes.

Investment Property Mortgage Interest

Mortgage interest on investment properties is treated very differently.

Instead of being an itemized deduction, it is considered a business expense reported on Schedule E against rental income.

This allows investors to deduct a wide range of operating expenses, including:

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Property management fees

- Depreciation

There is no $750,000 cap on interest deductions for investment properties. Interest is treated as a normal operating expense.

Form 1098 and Mortgage Interest

Most borrowers receive Form 1098 from their lender each year. This form reports the total mortgage interest paid.

Key things to know:

- Lenders send a 1098 only if more than $600 of interest was paid

- The form is informational and not strictly required to claim the deduction

However, it makes tax filing easier and provides documentation in case of an audit.

Timing of Mortgage Interest Deductions

Mortgage interest is deducted based on when it is paid, not simply when it accrues.

- You can only deduct interest that was paid during the tax year

- A payment made in January typically applies to interest accrued in the prior year

- Example: A January 2025 payment usually covers 2024 interest, but is deducted in 2025

Prepaying interest does not change this rule. Interest must relate to periods that have already occurred in order to be deductible.

If you do not receive a 1098

You can still document mortgage interest using:

- Monthly mortgage statements

- Payment history from the servicer

- Loan servicing summaries

- Closing documents or Closing Disclosure

If your loan was transferred between lenders during the year, you may receive multiple 1098 forms, which is normal.

Prepaid Interest at Closing

Interest paid at closing, often called prepaid interest, is deductible in the year it is paid.

This amount usually appears on:

- Form 1098

- The Closing Disclosure

If you did not receive a 1098, the Closing Disclosure can serve as documentation.

One Important Reality

Many homeowners assume the mortgage interest deduction significantly reduces their taxes. In practice, most homeowners do not benefit from it because the standard deduction is so high.

If your combined itemized deductions do not exceed the standard deduction, the mortgage interest does not provide a tax advantage.

❗ Disclaimer: UnrealFi does not provide tax advice. Always consult a qualified tax professional regarding your specific situation.